34 Effects of Globalization

Globalization is not a fundamentally new invention of the post-Reagan era. However, the increase of the technical possibilities of both, the actual transportation of goods, as well as the practical with the speed of light transportion of intangible benefit and pecuniary papers through the computerized trading is concerned, new possibilities, both quantitatively and qualitatively, have been opened. The main effect of globalization, or more generally internationalization, lies in the fundamental fact to at least temporarily generate an unbalanced foreign trade balance. Such a foreign trade surplus or deficit can be, in principle, both on goods and services in GDP's as related to capital as well.

In our

system of equations this is considered with the terms![]() and

and![]() :

:

![]() and

and

![]()

In principle this can be extended to the entire world economy by the following System of Differential Equations

![]() and

and ![]() (34.1)

(34.1)

wherein the sizes of![]() and

and![]() considere the

mutual interactions of the i-th with the j-th economy.

considere the

mutual interactions of the i-th with the j-th economy. ![]() is then the net

inflow or outflow of GDP without payment,

is then the net

inflow or outflow of GDP without payment, ![]() then

is the net capital inflow or outflow without GDP trade-off. Inflow or outflow

can be distinguished by the sign. The world economic system is then solved in

principle by the maximal

then

is the net capital inflow or outflow without GDP trade-off. Inflow or outflow

can be distinguished by the sign. The world economic system is then solved in

principle by the maximal![]() dimensional

matrix

dimensional

matrix

![]() and

and ![]() (34.2).

(34.2).

The occurring determinig matrices need not

always be diagonal. Thus, for example, in![]() in

addition to natural population growth can be incorporated known migration of

people. And also other interactions between the economies of the world in the

other coefficient matrices, which naturally should also include the impact of

the monetary exchange rates around. The practical forecasting abilities of such

a model are only limited by the computational effort and the reliable

determination of the raw data to fill the coefficient matrices. This considerable

hard work we can not do yet, especially because the freely available data bases

rarely give reliable input to pay respect to the above defined foreign

entanglements. Instead, we give an example of two linked dummy economies. What

we should also be aware of is, that an international exchange of money in

trade-off for GDP changes not much in the balance of a national economy (

in

addition to natural population growth can be incorporated known migration of

people. And also other interactions between the economies of the world in the

other coefficient matrices, which naturally should also include the impact of

the monetary exchange rates around. The practical forecasting abilities of such

a model are only limited by the computational effort and the reliable

determination of the raw data to fill the coefficient matrices. This considerable

hard work we can not do yet, especially because the freely available data bases

rarely give reliable input to pay respect to the above defined foreign

entanglements. Instead, we give an example of two linked dummy economies. What

we should also be aware of is, that an international exchange of money in

trade-off for GDP changes not much in the balance of a national economy (![]() and

and![]() are initially

defined without direct trade-off). It is given for the usual foreign trade

(represented by large identifiers:

are initially

defined without direct trade-off). It is given for the usual foreign trade

(represented by large identifiers:![]() and

and![]() ):

):

![]() and

and

![]()

![]() and

and

![]()

(34.3)

If there are only two economies and in the event of a balanced trade is given:

![]() and

and ![]()

![]() and

and ![]()

(34.4)

where the bracketed values are always zero. And thus results once again in the undisturbed basic equations, as the net effect vanishes. In the case of an unbalanced trade, but this is not zero, and if j sold to i the net quantity B, we get:

![]() and

and ![]()

![]() and

and ![]()

(34.5)

The resulting imbalance is uncomfortable, because now the capital stock of i decreases with increasing GDP, while the reverse is true at j, a rising stock of capital at a reduced offer of goods. In general, one would have to expect a deflation with i and an inflation with j. To maintain a general stability that is at least an approximate balance in foreign trade relations is desirable. For the economy j but the problem is surprisingly greater, because it is difficult to replace the missing GDP. On the other hand i has a relatively low problem: it can close the small gap in the balance sheet, which only adds up to her, through additional value-free money creation comparatively easy. This can be money creation through the printing press, or by the formation of new financial derivatives. So we can open the following equation

![]()

with a GDP of ![]() (34.6),

(34.6),

from which the balance of i is

compensated without it is to be expected that inflation or deflation occurs

over the normal level. It has, however, a different problem: you have to sell

financial derivatives. On the one hand, on its own population, but this reduces

their purchasing power for its own GDP. Buyers would be better from the outside

to absorb these derivatives. Economy i can try to sell these financial

products worldwide so that its internal capital increases. In the most

unpleasant case now even j buys these derivatives worth![]() , but j has to

provide i the corresponding of GDP for this: Due to

, but j has to

provide i the corresponding of GDP for this: Due to

![]() and

and

![]() with the amount of currency

with the amount of currency ![]() equity, then holds:

equity, then holds:

![]() and

and ![]()

(34.7)

Because most of the money creation by i is next-year, the effect is not quite so strong, so that instead of a factor 3 one should estimate76 about a factor of about 2. The situation but worsens considerably for j.

The bottom line is: If two economies in mutually strongly unbalanced exchange with each other, then the negative effects are multiplied for the one economy, which exports its GDP to the same economy it buys financial bonds from. Globalization of trade and financial flows can thus quickly have significant consequences for unbalanced economies. The net differences

![]() and

and ![]() (34.8)

(34.8)

we can again express as our freely definable![]() and

and![]() coefficients. The

following model calculation, we are now taking the less serious case that only

a third country takes such financial securities. This happens for example when

a national finance incorporates extra national funds into domestic financial

system. This is done within the framework of international stock markets in the

modern globalization very easily. It applies in this case, without regard to

population growth:

coefficients. The

following model calculation, we are now taking the less serious case that only

a third country takes such financial securities. This happens for example when

a national finance incorporates extra national funds into domestic financial

system. This is done within the framework of international stock markets in the

modern globalization very easily. It applies in this case, without regard to

population growth:

![]() and

and

![]()

![]() and

and

![]()

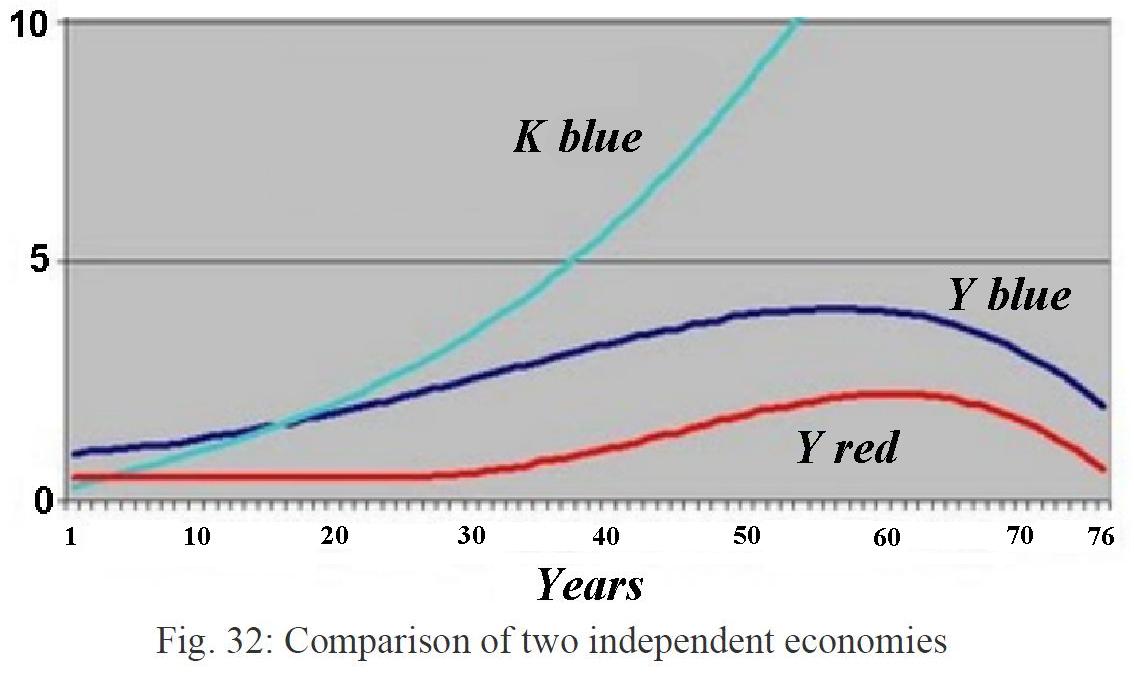

In the

first graph we see, only for comparison with the following second graph, the

case![]() without such an

interaction: Both economies take the usual course of their development of the

GDP (the capital stock is in the graph given only for blue, here are interested

in essentially the both GDP's). We assume in the model that the red economy

starts 25 years later, and is only half as strong as blue. The maximum of the

GDP's of red remains well below the maximum of blue, as to be expected.

without such an

interaction: Both economies take the usual course of their development of the

GDP (the capital stock is in the graph given only for blue, here are interested

in essentially the both GDP's). We assume in the model that the red economy

starts 25 years later, and is only half as strong as blue. The maximum of the

GDP's of red remains well below the maximum of blue, as to be expected.

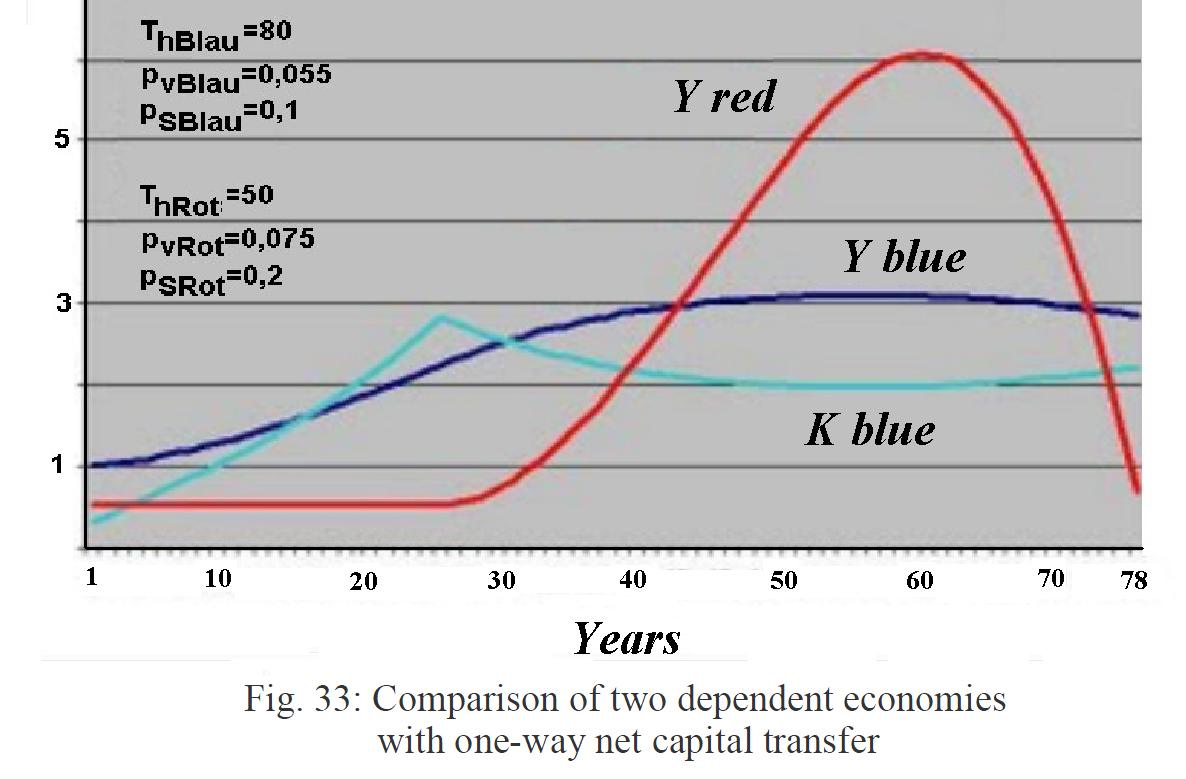

In the second graph we see the significant effect of such a capital transfer in an amount equal to one tenth of the GDP of Blue: Now, while red dramatically increases and the GDP of blue even gets overhauled, the GDP of blue stagnates at a pretty good level. But also evident is, that now Red crashes earlier and far more violent, because of the disproportionately high stock accumulation. At the same time can make it Blue over much longer periods than usual to keep "afloat". And this will happen as long as Blue can internationalize its surplus funds by selling them abroad.