20 Rule of Thumb: the Economic half-life Time

Already in the measured values for the

investment banking industry a certain half-life can be seen. So we ask

ourselves what such dynamic effects are a result of and whether there is a way

to estimate such times, at least roughly. Thus we consider the following highly

simplified model of a closed economy: An economy has the economic performance![]() given to a start

time. Whereas a lot of money

given to a start

time. Whereas a lot of money![]() is delivered.

is delivered.![]() is slightly

larger than

is slightly

larger than![]() , so that all

things can be paid for with money in circulation

, so that all

things can be paid for with money in circulation![]() ,

as well as a general reserve asset

,

as well as a general reserve asset![]() can

be accumulated:

can

be accumulated:

![]() (20.1)

(20.1)

With the growth of the economy now is growing the capital stock. Thus we can write

![]()

![]() (20.2)

(20.2)

It is considered that

arises more money with the economic growth41![]() , and the

inflation rate

, and the

inflation rate![]() becomes effective

and, finally, the deposits with the banks earn

becomes effective

and, finally, the deposits with the banks earn![]() of interest. We compute, as always, on an annual basis

of interest. We compute, as always, on an annual basis![]() , therefore the

time factor

, therefore the

time factor![]() is the number of

years. We are now following the question: At what juncture

is the number of

years. We are now following the question: At what juncture![]() is the capital

stock greater than the sum of tradable goods? So mathematically, the

inequality:

is the capital

stock greater than the sum of tradable goods? So mathematically, the

inequality:

![]() (20.3) ?

(20.3) ?

Now, the relative share of capital stock at all levels of the economy, goods and assets, results from the ratio of capital stock to total national wealth

![]()

(20.4)

and to reduce the fracture results in

![]() (20.5).

(20.5).

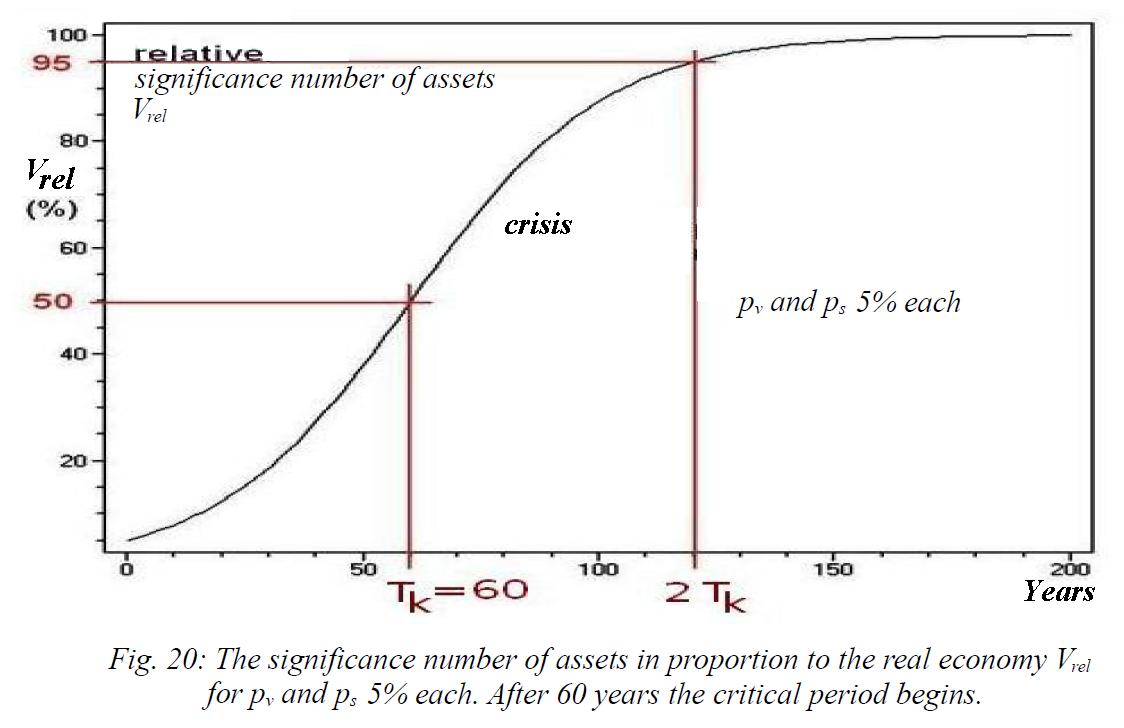

This gives a dimensionless

value that is called the "significance number" of capital in an

economy. When this value gets greater than 0.5 = 50%, so there will be a

transition, after which the meaning of production falls behind the financial

sector . This equation can now be easily resolved to the critical time ![]() , as in the case of equality holds

, as in the case of equality holds

![]() (20.6)

(20.6)

and thus after a short algebra we get

(20.7).

(20.7).

As is![]() , one can also

see that the critical time

, one can also

see that the critical time![]() goes

to infinite for

goes

to infinite for![]() or

or![]() , which

corresponds to a stable system. Typical values for the savings rate and

interest rate are about 10% and 5% in the FRG. This gives a critical time of

, which

corresponds to a stable system. Typical values for the savings rate and

interest rate are about 10% and 5% in the FRG. This gives a critical time of

![]() years.

years.

For moderate values, about 7% and 3%, the corresponding time is

![]() years,

years,

which is already more than

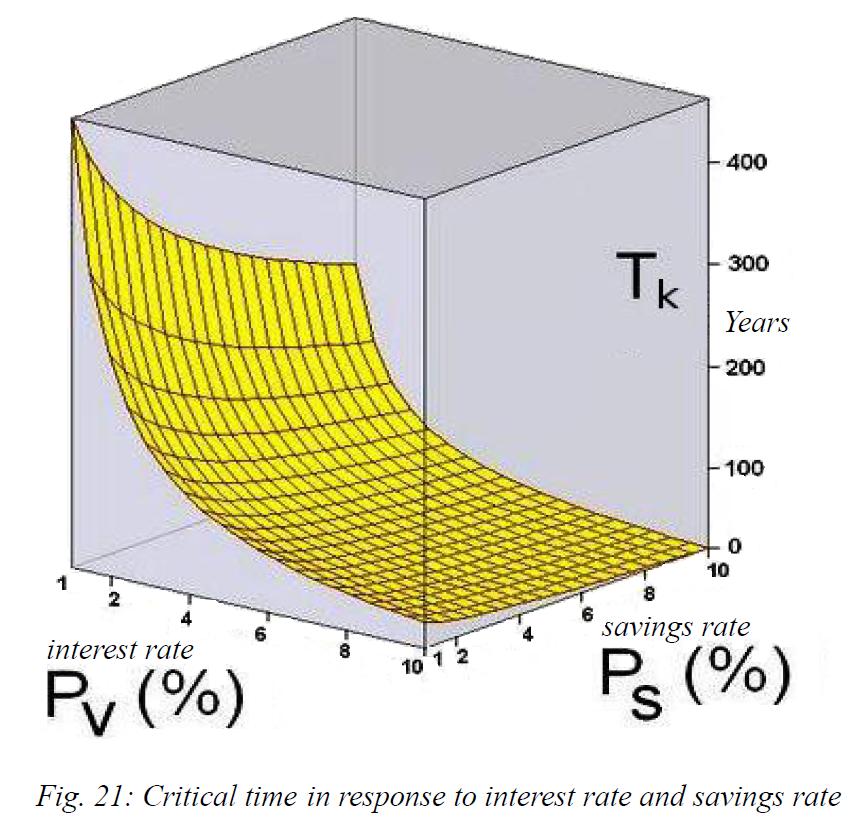

two generations. The critical time of a monetary economy depends so much on the

return on investment: With every percentage point it drops considerably.

Somewhat less strongly is the influence of the savings rate. With only 1% for

each![]() and

and![]() , the critical

time is more than 400 years. An increase in interest rates to 10% results in a

lifetime of only a few decades. An increase in the savings rate alone to 10%

reduced but this time not much, it is then still almost 300 years. At moderate

values of

, the critical

time is more than 400 years. An increase in interest rates to 10% results in a

lifetime of only a few decades. An increase in the savings rate alone to 10%

reduced but this time not much, it is then still almost 300 years. At moderate

values of![]() and

and![]() the critical

period is therefore from

the critical

period is therefore from

![]() years.

years.

The rule of thumb for the

critical period can be reduced to a simple rule because of the shallow curve of

the natural logarithm. As![]() and

and

![]() are significantly

smaller than one and commute to values of about 5%=0.05, one can roughly

approximate:

are significantly

smaller than one and commute to values of about 5%=0.05, one can roughly

approximate:

![]() and

and

![]() (20.8).

(20.8).

So that we can remember as a "raw rule of thumb" for the average lifetimes of capital driven economies:

![]() (20.9).

(20.9).

With average interest rate on all assets of about 5%, we obtain for example

![]() years (20.10)

years (20.10)

magnitude as for the estimation of the saturation level.